March 22, 2026 | Jonathan Bird

How Much Do You Really Need to Retire? It Depends on One Thing.

Most people ask the wrong question. They want a magic number — some savings target they can hit and finally feel ready. But that framing is exactly what leads people to work a decade longer than they need to, or worse, run out of money at 80.

The right question isn't how much do I need? It's when do I want to retire, and how long does my money need to last?

There Is No Universal Number

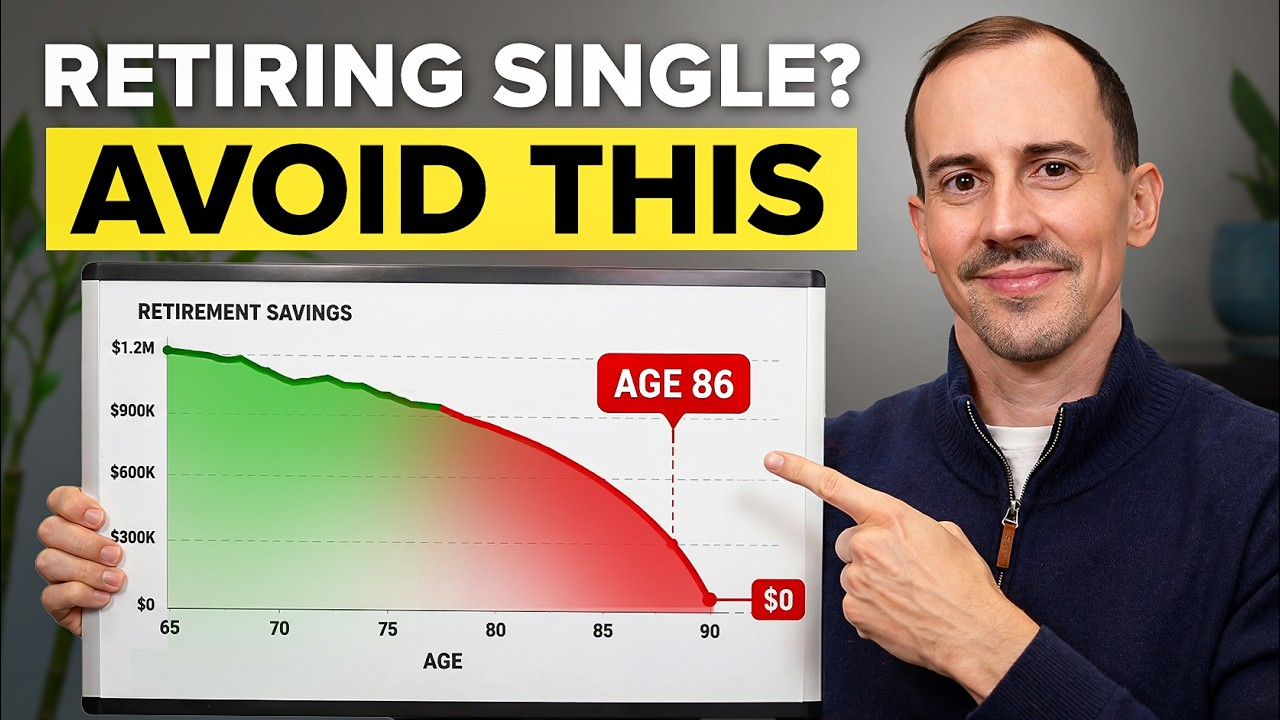

Here's the range in practice, all targeting $100k/year in retirement spending:

- $130,000 in savings — if you retire at 70 with maximum Social Security and only need your portfolio to last 12 years

- $1,000,000 — if you retire at 65 and plan through 88

- $3,500,000 — if you retire at 55 and plan through 100

Same lifestyle. Wildly different targets. Time horizon controls everything.

Your Portfolio Only Has to Fill the Gap

Before panicking about your savings balance, figure out what income you already have coming in — Social Security, a pension, rental income. Your portfolio only needs to cover the difference between that income and your actual expenses. For some people, that gap is small. For others, it's enormous. Most people never calculate it.

The Three Phases of Retirement

Retirement isn't one long, uniform stretch. It has three distinct phases that carry very different financial demands:

Early retirement (pre-Medicare, pre-Social Security) is the most expensive. You're funding everything yourself, you're likely most active, and you're maximally exposed to sequence of return risk — which we'll get to in a moment.

Traditional retirement is when the pieces start working together. Social Security kicks in, Medicare begins, and guaranteed income creates a floor under your spending.

Late retirement often brings lower day-to-day expenses, but longevity and healthcare costs introduce new uncertainty. This is not the time to run short.

Two Mistakes That Break an Otherwise Good Plan

1. Sequence of return risk. A bad market in your first few years of retirement can permanently damage a portfolio — even if long-run returns look fine on paper. The solution is a "castle and moat" approach: keep a buffer of stable, liquid assets separate from your growth portfolio so a downturn doesn't force you to sell at the worst possible time. Don't assume you'll be the exception. You won't be.

2. Unexpected expenses. Healthcare costs, a home repair, helping a family member — unplanned spending derails more retirements than bad markets do. A solid plan accounts for this explicitly, both in your budget and your portfolio construction.

The bottom line: $100k a year in retirement is achievable across a wide range of situations — but only if you build your plan around your actual timeline and close your actual gap. Generic rules and average survey numbers aren't your plan. They're just noise.